Party Like It's 1929!

The oligarchs of Silicone Valley and the Magnificent 7 have inflated a circular financing AI bubble of epic proportions. When the music stops, trillions in faux valuations will vanish.

After nearly two decades of misguided policies by the U.S. Federal Reserve and other G7 central banks planners, and bailouts for billionaires alongside unlimited money printing since the Great Financial Crisis, one must ask: Were any lessons learned? Why are we trusting the arsonists who ignited the blaze to extinguish it? Does anyone really believe that valuations no longer matter?

Today, the U.S. economy is the strongest in the world. The EU and UK are headed for a massive energy crisis. They have committed economic suicide through Net Zero zealotry and open borders. The AI mania will drive energy costs even higher.

China’s economy looks grim. Its shadow banking sector and housing bubble are on the brink of disaster. China is headed for an economic shock as its shadow banking system and housing bubble slide toward an abyss. Yet China continues to build two coal-fired power plants a week. In contrast, UK and EU citizens face record energy prices and rising business bankruptcies. Still, UK and EU rulers press forward with climate policies no one voted for.

The U.S. Federal Reserve’s monetary policy and other central banks’ planners’ policies cannot address supply-chain disruptions caused by a lack of oil by simply raising interest rates. Nor can they print oil or AI chips, as they did with decades of stealth Quantitative Easing, which inflated central banks planners' balance sheets and sparked today’s inflation.

We expect Oil prices to remain trading in the $100-$120 range until the Strait of Hormuz is resolved. It’s critical to note that monetary policy cannot resolve an oil supply shock; if interest rates rise, it will ignite a liquidity crisis in private credit, commercial, and residential real estate markets. The inflationary blaze ignited under Biden, his Inflation Reduction Act, and his declaration of war on fossil fuels, which saw a 40-year-high inflation rate of 9.1% and gasoline prices 25% higher than today’s.

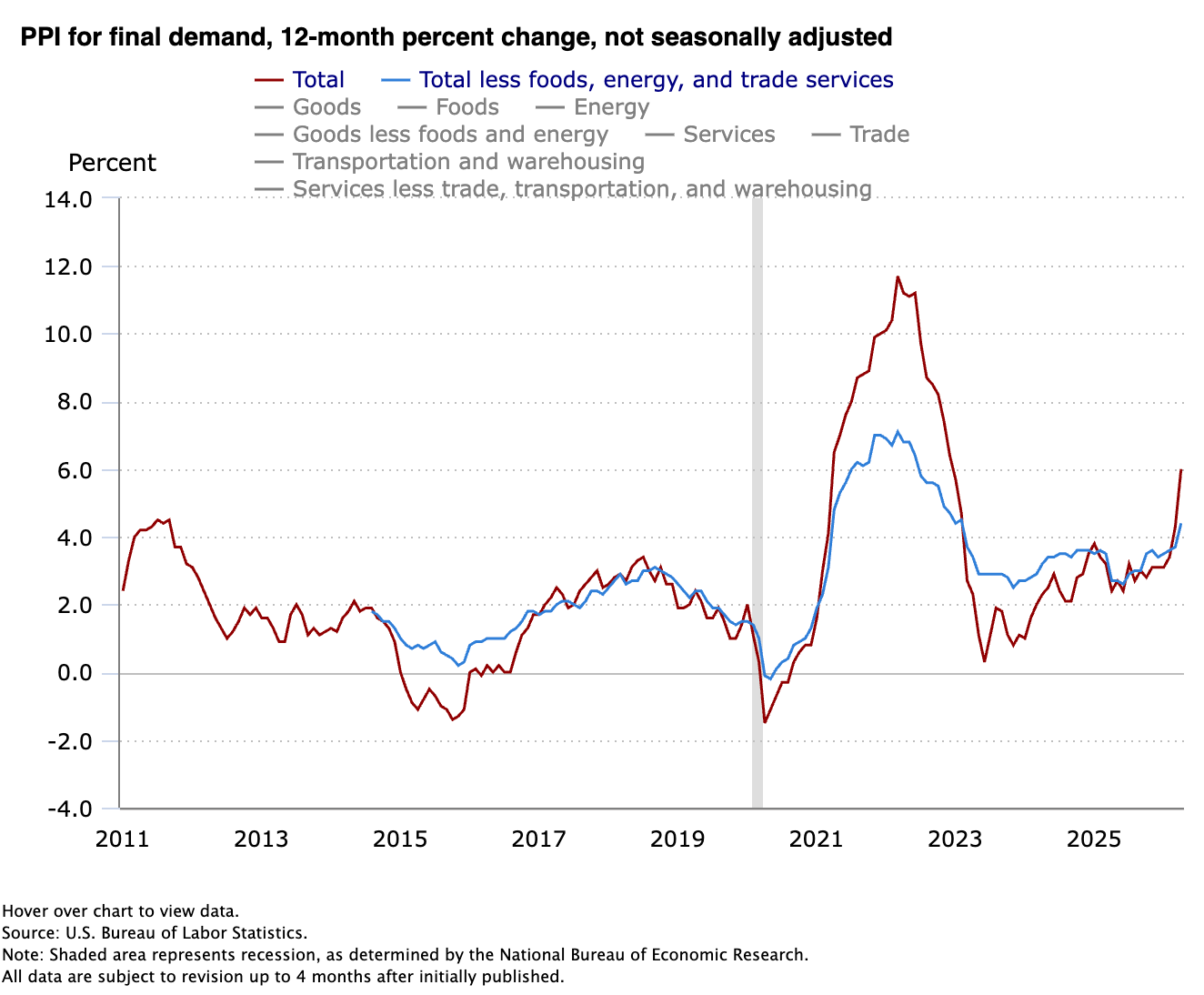

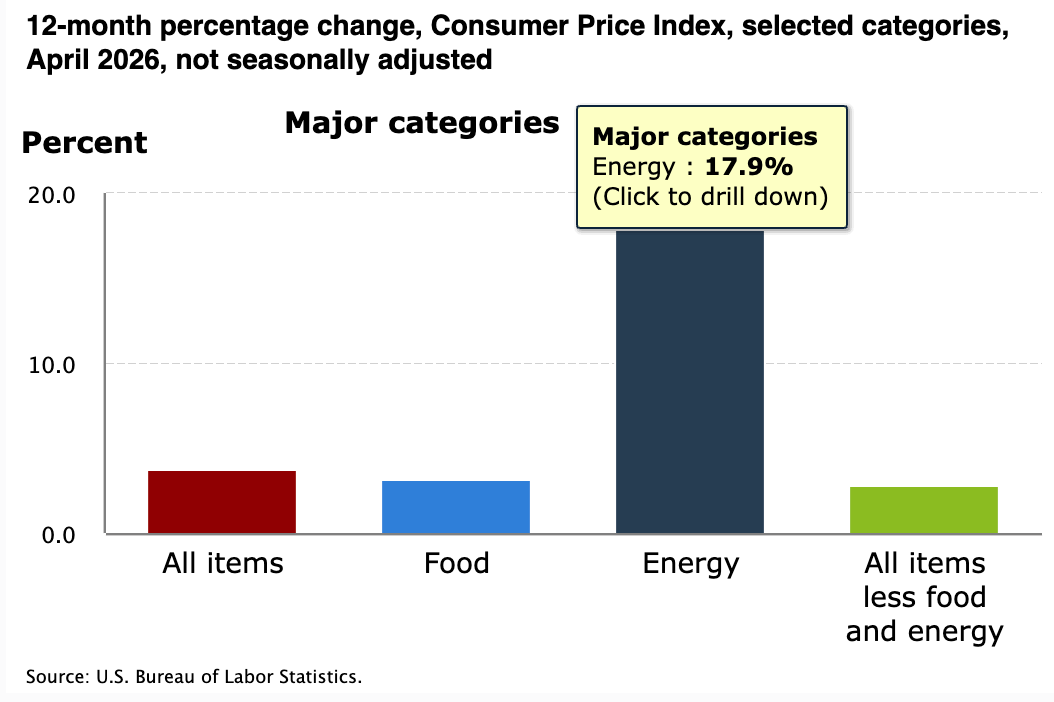

This week, the U.S. Consumer Price Index (CPI) and the Producer Price Index (PPI) both came out “hot” – higher than market expectations, caused by the surge in energy prices and supply chain disruptions. This months data led many talking heads to speculate that the Federal Reserve and other central banks planners would jawbone about the potential need to raise interest rates. I disagree with this thesis.

The recent inflation surge, as reflected in the CPI below and the PPI above, is driven by a supply shock stemming from the situation in Iran, and tightening monetary policy is not a viable solution.

We have not seen meaningful corrections in the stock or bond markets in decades. The Federal Reserve’s policy failures under Greenspan, Bernanke, Yellen, and Powell have been extraordinary. The Fed has doubled down on what it knows: misguided money printing and policy drift away from price stability and full employment, sliding down the slippery slope towards DEI, Equity, Climate Change, as they inflate everything bubbles. Biden’s passage of the Inflation Reduction Act put the nail in the U.S.’s economic coffin, further exacerbating inflation to 40-year highs and marking a tipping point that created many of today’s problems, as seen in the above charts.

The Iran oil-driven price shock is different. While the recent, temporary surge in oil prices is transitory, there are many other elephants in the room, caused by the central planners that nobody wants to acknowledge.

Concentration Risk is not priced into today’s irrationally exuberant markets and is a massive problem.

As for the AI bubble, Nvidia shares have risen 44% since the end of March. has surged by $1.7 trillion. Google shares have increased by nearly 50%, raising the company’s market cap by $1.5 trillion. The market cap of those two companies increased by $3.2 TRILLION in less than two months. You could buy almost 15 Citibanks for the increase in market caps! NVIDIA reached a new high of $236.54 per share and a market cap above $5.8 trillion. Google’s stock traded above $406, with a market cap of over $5 trillion.

Are we witnessing an AI mania?

The sample below shows a huge contrast: market capitalizations of profitable banks and corporations versus the above Magnificent 7’s bloated, fantasy-based valuations, completely detached from real revenues.

• Bank of America Corp. (BAC) — $353.41 billion

• Morgan Stanley (MS) — $304.88 billion

• Goldman Sachs Group, Inc. (GS) — $280.99 billion

• Citigroup Inc. (C) — $210.92 billion (global IB and markets focus via Citi)

• Micron Technology (MU) — ~$832 billion

• Eli Lilly (LLY) — ~$901 billion

• Walmart Inc. (WMT) — ~$1.054 trillion

• Berkshire Hathaway Inc. (BRK.B) — ~$1.048 trillion

Since the end of March, the UK 10-year yield has surged 22%—from 4.21% up to today’s high of 5.19%. This week, a U.S. 30-year bond auction came in at 5.046%. Two data releases were delayed after some market participants deemed them inflationary. Japan’s bond yields are surging as its currency declines.

The bond markets are signaling that something is very wrong. U.S. ten-year bonds are a terrific buy at 4.60% - and tech stocks are a SELL, SELL, SELL.

Elon Musk’s estimated $2 trillion SpaceX IPO in June may define the peak of AI mania.

In summary, we are witnessing a convergence of unsustainable trends—rising debt, reckless monetary policies, energy shocks, and speculative technology manias—that cannot continue indefinitely. Investors, policymakers, and business leaders must recognize the growing risks beneath the market’s irrational exuberance. A return to fundamentals, prudent risk management, and clear-eyed realism will be essential to weather the coming crisis. It is extraordinary how the AI circular financing bubble keeps inflating at breakneck speed as it hurtles toward disaster! The broader economy will soon learn what happens when the AI gold rush turns into an AI bloodbath.